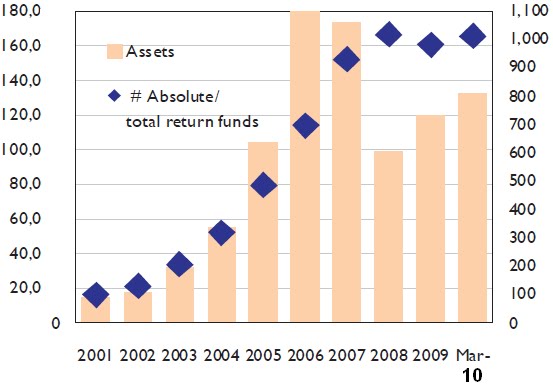

Assets Under Management (in €bns. lhs) and Numbers of Absolute Return

and Total Return Funds (rhs)

In the first quarter, they attracted net inflows of €9.7bn compared to €11bn during the whole of last year. According to Lipper, for investors, the attraction of the funds has been boosted by a combination of low interest rates, economic uncertainty and stock market volatility. “Among product providers, hedge fund managers see absolute return funds as an opportunity to move into the mainstream mutual fund market, though figures show that the most successful funds are from fund managers with a foot in both camps,” states Lipper.

As a group absolute return funds aim to achieve positive returns in all market conditions, but they can have different types of exposure in order to achieve it. They invest through a variety of investment strategies in domestic equity or bond markets, or sectors such as commodities, while others have a global spread and hold a broad range of assets. It is particularly noteworthy that absolute return bond funds sold particularly well during the first quarter as investors sought out higher yields. Indeed seven of the best-selling absolute return funds in the first quarter were bond funds.

The popularity of bond absolute return funds suggests that these are retail and/or distributor/advisor products. The top selling products were from, in order, Standard Life, Julius Baer, UBI Pramerica, JPMorgan, Schroder, and in aggregate the largest asset managers in absolute return and total return funds are shown in the table below:

Top Five Groups by Assets in Absolute Return/ Total Return Products

as at End March 2010

The names that have cropped up each have strong branding, and excellent distribution capability, providing supporting evidence that these are retail products rather than products that are invested in by institutions. This point is reinforced by the fact that the UK and Italy together make up 40% of the sales by end market – territories with strong IFA and bank networks for distribution, respectively.

Some absolute return funds are described as Newcits, principally those launched by hedge fund managers. Lipper suggest that more than half of European hedge fund managers have launched, or are planning to launch a Newcits product. Given that the market is for retail products, the sales represent a new end-market for hedge fund groups and therefore represent incremental business. The power of branding in retail channels would itself reinforce the concentration in the hedge fund business – the bigger funds taking an increasing share of the industry through time.

No comments:

Post a Comment